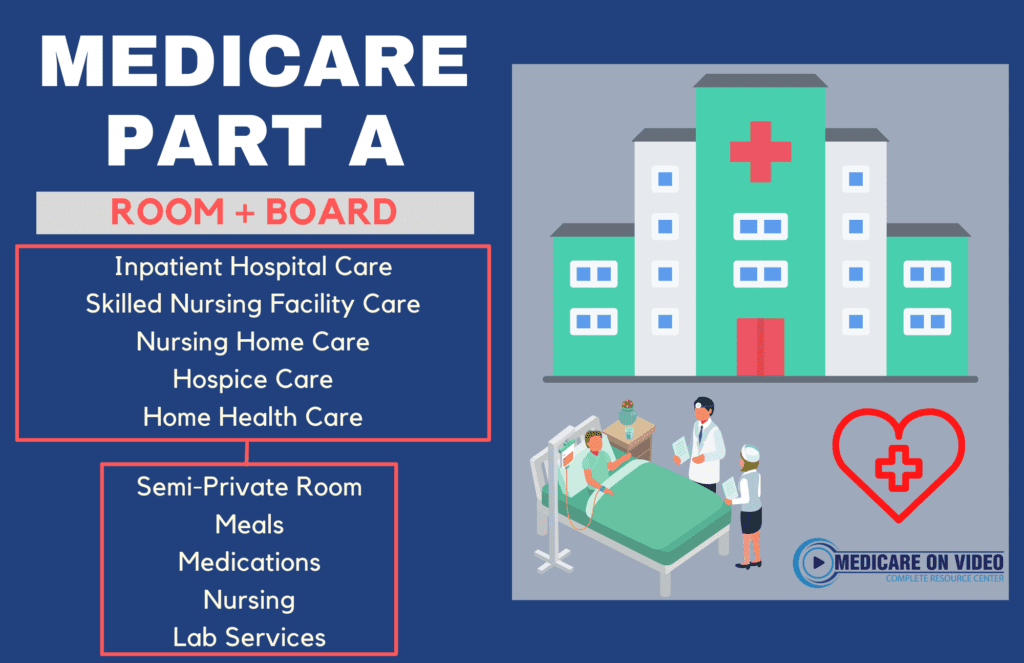

Medicare Part A is a program that helps pay for hospital stays. You can consider Part A your “room and board” in the hospital, including things such as a semi-private room, meals, medications, and nursing care.

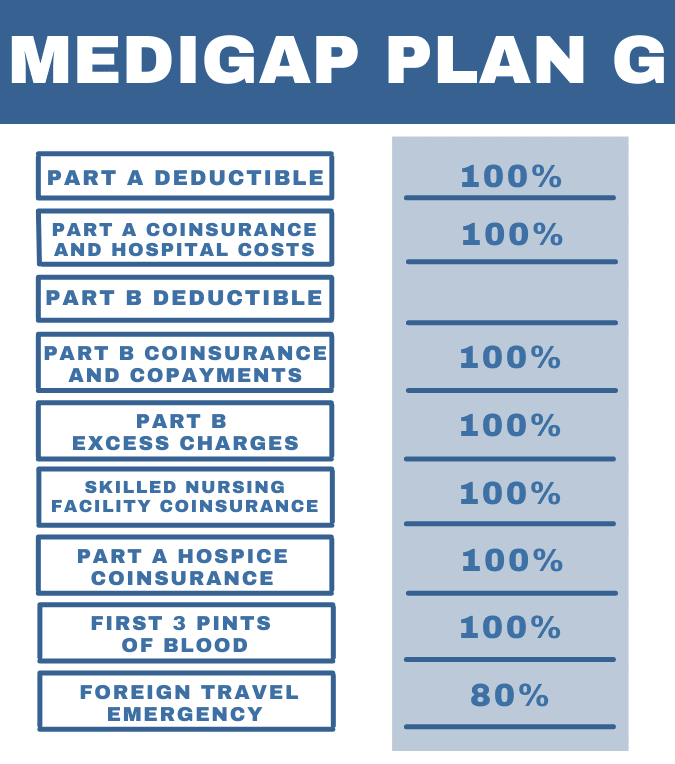

When you enroll in Medicare, your coverage will be automatic enrollment in just Original Medicare, unless you choose to sign up for extra benefits, such as Medicare Supplement Plan G. There are no deductibles or copays when using Original Medicare with Medigap G for hospital care.

What are the Pros and Cons of Medicare Part A?

Pros: It is one of the two main parts of traditional Medicare and has extensive coverage. This includes hospitalization, skilled nursing facility care after being discharged from the hospital, hospice care for terminal illnesses and some home health services

Cons: The deductible and coinsurance can be expensive so it’s important to find out if the Medicare supplement plan you’re considering will be able to cover these costs.

How Much does Medicare Part A cost?

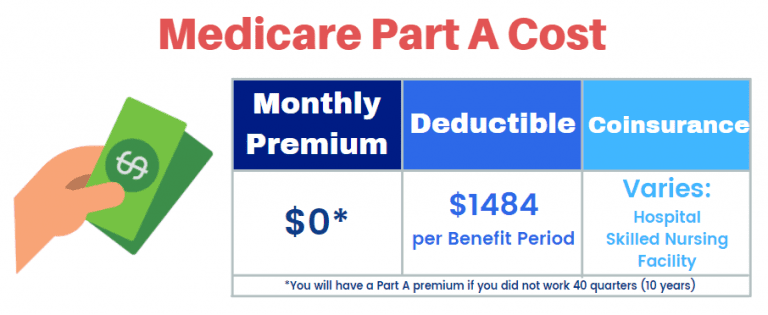

Medicare Part A typically has no monthly premium for most people. If you have worked at least 40 quarters (10 years), you are eligible for premium free Medicare Part A. If you have not worked the required 40 quarters, you will pay a premium for Medicare Part A depending on the amount of quarters you worked. In 2021, if you worked 30-39 quarters, you will pay $259 per month for Part A. If you worked less than 30 quarters, you will pay $471 per month for Part A.

Although most people do not have a monthly premium for Medicare Part A, there are other costs associated. Part A has a deductible of $1,484 (in 2021), as well as coinsurances for hospitalizations, skilled nursing care, hospice, and home health care. Medicare Supplement plans, such as Plan G, can cover these costs, leaving you with minimal out-of-pocket expenses.

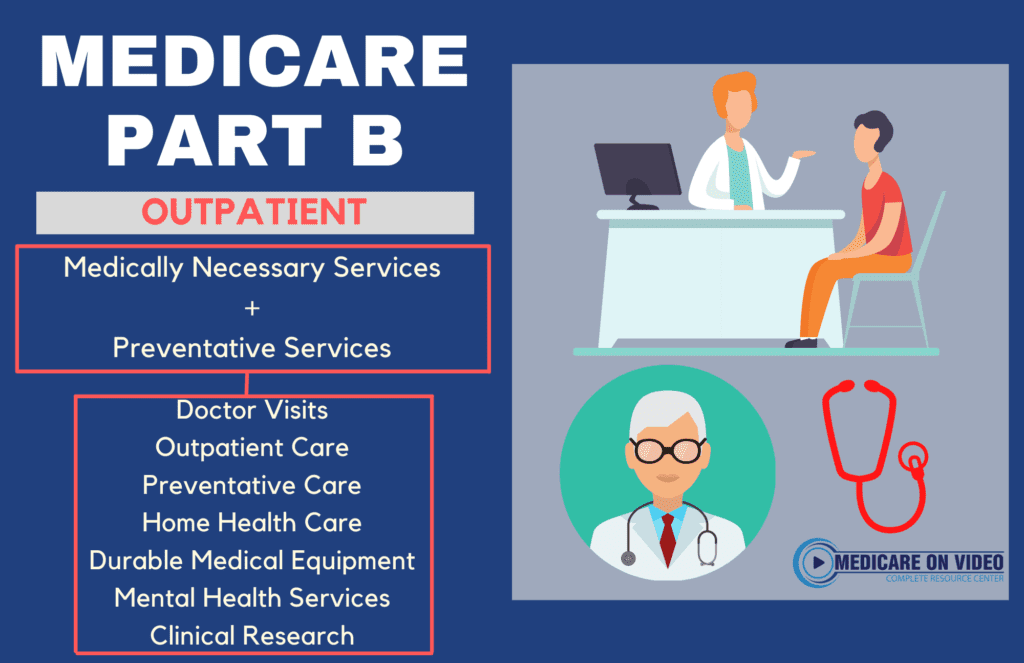

Medicare Part B is the counterpart to Medicare Part A under Original Medicare. This part of Medicare is considered your outpatient coverage. Part B covers outpatient care like lab work, x-rays and visits with your primary physician. It also includes coverage for these types of providers after being discharged from a hospital.

Coverage under Part B falls into two categories: medically necessary services and preventive services.

What are the Pros and Cons of Medicare Part B?

Pros: Medicare Part B provides extensive coverage for outpatient services. This coverage includes physician visits (primary and specialist), as well as procedures and assessments.

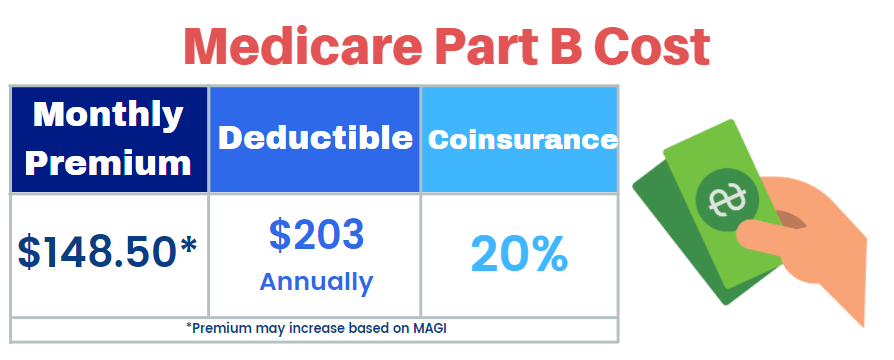

Cons: Medicare Part B does not cover 100% of your outpatient costs. There is an annual deductible of $203 (in 2021), as well as 20% cost-share if all medically necessary services. The 20% coinsurance, however can will be covered under a Medigap plan like Plan G.

How much does Medicare Part B cost?

Unlike Medicare Part A, Medicare Part B does have a monthly premium. In 2021, the standard monthly premium for Medicare Part B is $148.50. This premium, however, can increase based on your income from the last two years. If you made a higher modified adjusted gross income (MAGI) than the standard level of Medicare beneficiaries, you will pay a higher premium for Part B. The higher premium number is dependent on exactly what your MAGI was from two years ago.

You can enroll in Plan G at any time during the year. There is no open enrollment period for Medicare Supplement plans. If you are new to Medicare, you want to enroll into Plan G when your Part B begins to avoid any gaps in coverage. If you are already enrolled in Medicare, you can apply for Plan G during any month of the year, but must be able to pass medical underwriting. If you are currently enrolled in a Medicare Advantage Plan, you will want to wait until the Annual Election Period, also known as open-enrollment, to apply.

You can enroll in Plan G at any time during the year. There is no open enrollment period for Medicare Supplement plans. If you are new to Medicare, you want to enroll into Plan G when your Part B begins to avoid any gaps in coverage. If you are already enrolled in Medicare, you can apply for Plan G during any month of the year, but must be able to pass medical underwriting. If you are currently enrolled in a Medicare Advantage Plan, you will want to wait until the Annual Election Period, also known as open-enrollment, to apply.