Every year, January 1st marks the first day of Medicare’s General Enrollment Period, also known as the GEP. There are several Medicare enrollment periods that are important to all beneficiaries, but the GEP is directed at individuals who delayed enrollment past their Initial Enrollment Period (IEP) and don’t qualify for a Special Enrollment Period (SEP).

Let’s talk about the GEP and who should be enrolling in Medicare during this time.

General Enrollment Period Eligibility

The GEP occurs from January 1 – March 31 every year. During this time, you can enroll in Original Medicare, which consists of Medicare Parts A and B. You can also begin your enrollment into other types of Medicare coverage, but you must start with Parts A and B.

You are first eligible to enroll in Medicare during your Initial Enrollment Period (IEP). Your IEP begins three months before the month of your 65th birthday, includes the month of your birthday, and concludes three months after your 65th birthday. For example, if your birthday is October 5th, your IEP begins July 1st (3 months prior to your birthday) and ends January 31st (3 months following your birthday).

Some people choose to delay their Medicare enrollment past their IEP. The main reason for this is when someone has other coverage through an employer – either their own employer or their spouse’s. If the employer is subsidizing your health plan, it may be cheaper for you to stay on the group plan instead of transitioning to Medicare. As long as that coverage is creditable, you can delay enrollment without any penalties.

If you had creditable coverage, you will qualify for a Special Enrollment Period (SEP) when that coverage terminates. You’ll be eligible to enroll in Medicare for 6 months following that termination of your employer benefits.

However, if you delayed Medicare enrollment during your IEP and did not have other creditable coverage, you will not qualify for a SEP and must wait to enroll during the GEP. (There are other reasons you could qualify for a SEP, so talk to a licensed agent to see if any apply to you.)

If you enroll during the GEP, your effective date will not be until July 1 of that year. If you don’t have other coverage in place, this could mean an even longer lapse in coverage. You will also not be able to enroll in either a Medicare supplement plan or a Medicare Advantage plan until July 1.

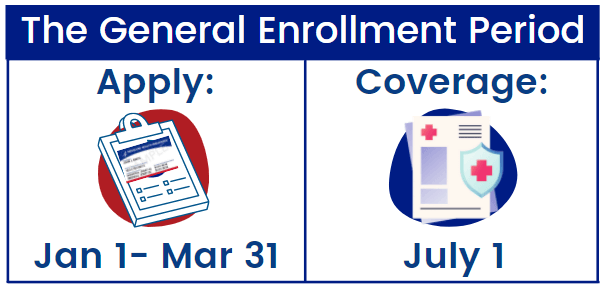

General Enrollment Period Timeline

The General Enrollment Period has a very strict timeline of both when you can apply and when your coverage will begin. The application period for the GEP takes place from January 1st- March 31st every year. The Medicare coverage, however, will not begin until July 1st. That’s right- although you must apply during the first three months of the year, your coverage will not begin until mid-year in July. There is no wiggle room, unfortunately, as the dates are set in stone.

General Enrollment Period Penalties

One more thing about the GEP: penalties. If you’re enrolling during this time, it’s likely that you’re going to be paying one or more penalties.

If you qualify for premium-free Part A, there is no penalty for delaying Part A. However, you will pay a penalty for delaying Part B. For every 12-month period that you delay coverage, you will pay a 10% penalty. (This does not apply if you qualify for a SEP.) The standard premium in 2022 is $170.10. If you missed just one 12-month period, $17.01 would be added to your monthly premium. You’ll pay that penalty for as long as you continue your Part B coverage.

Best Option for Applying for Medicare

It is best to avoid having to apply for Medicare during the General Enrollment Period whenever possible. Between the strict timelines and the late enrollment penalty, it is important to apply for Medicare during the other appropriate enrollment periods. If you have questions about which enrollment periods you may qualify for, give us a call at 877-885-3484.